So, is the Stock Market Overvalued?

21 May 2020

“A cynic is a man who knows the price of everything and the value of nothing.”

– Oscar Wilde

A host of financial news headlines suggests that investors are in the most overvalued stock market since the late 90s. “Wall Street Heavyweights Are Sounding Alarm About Stocks“, Bloomberg warned. And, from CNBC, “David Tepper says this is the second-most overvalued stock market he’s ever seen, behind only ’99“.

If the stock market were indeed overvalued, it would suggest that prices would soon be reverting to the mean. Investors could then expect more losses to come. But is this fear justified? How can we determine the real value of the market?

1. Use a Proper Valuation Metric

There are many ways to value your investments. The most common metric is the Price to Earnings ratio, which compares share prices against what a company actually earns. However, as earnings can swing wildly, determining a company’s earnings – typically over a 12-month period – can be a difficult and arbitrary affair.

You could look at their performance thus far, but this would not say much about their future performance. Alternatively, you could attempt to extrapolate their future earnings; but if the pandemic has taught us anything, it’s that you really can’t know what will happen even just one week from now.

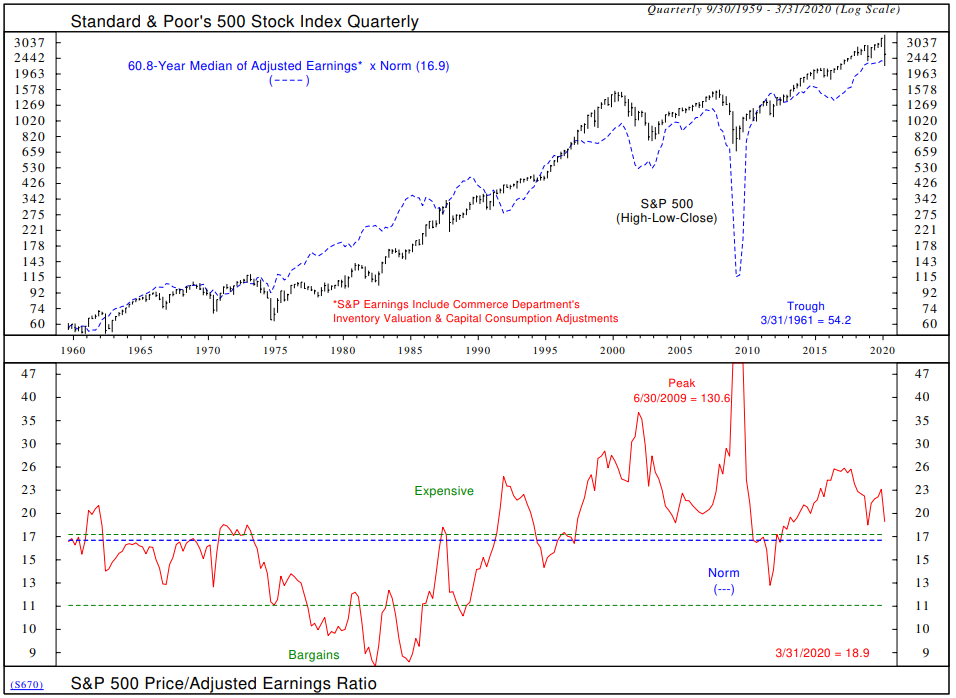

The chart below gives an example of a long-term P/E ratio for a common measure of US stocks. You’ll notice that the P/E ratios are all over the place, and spike dramatically during recessions as earnings plummet. The P/E peak was 130 in June 2009!

If you were an investor looking at that metric, you might thus have concluded that the markets were overvalued and held back from investing. However, June 2009 was 3 months after the stock market bottomed. Staying out for fear of overvaluation would have only made you miss out on some of the best gains in the market.

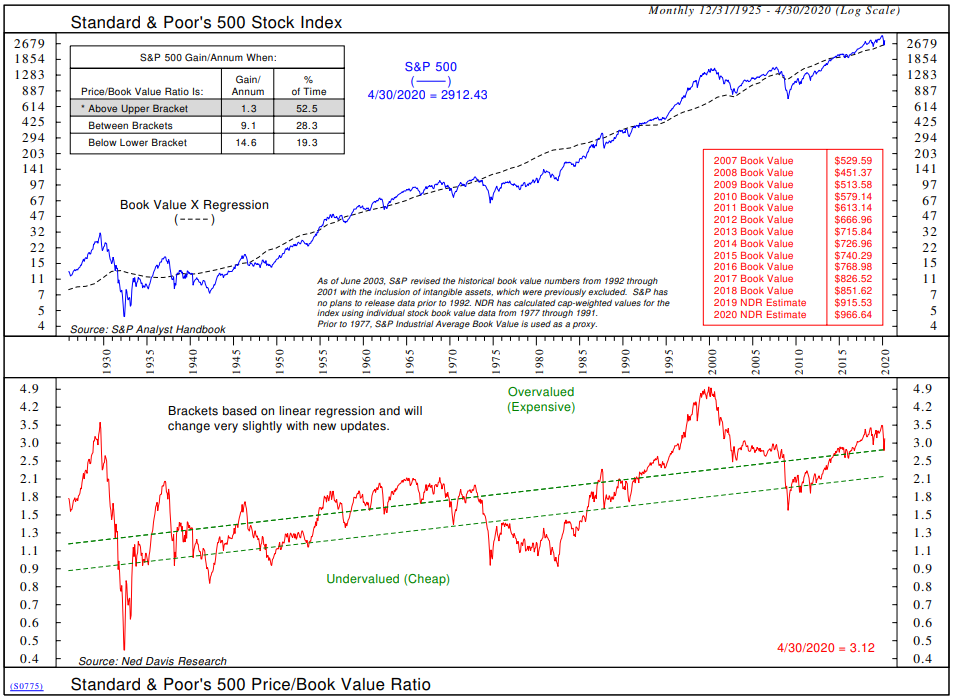

That’s why we consider the academic favourite of Price to Book ratio to be a much better valuation metric. A company’s book value is the total value of its assets minus its liabilities. This value is not as volatile as earnings, and gives you a much better idea of a company’s value. The Price to Book ratio is what we use to value the majority of our portfolios (and your investments).

The chart below shows how P/B value moves over time. You could argue that the US stock market is expensive. That’s why it’s important to be globally diversified, rather than fully invested in a singular country (or even several countries) that could expose you to unsystematic risk.

2. Can I Use a Valuation Ratio to Time My Investments?

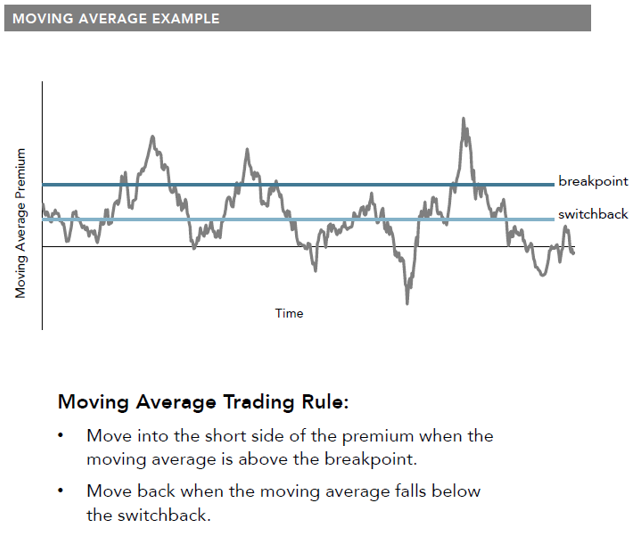

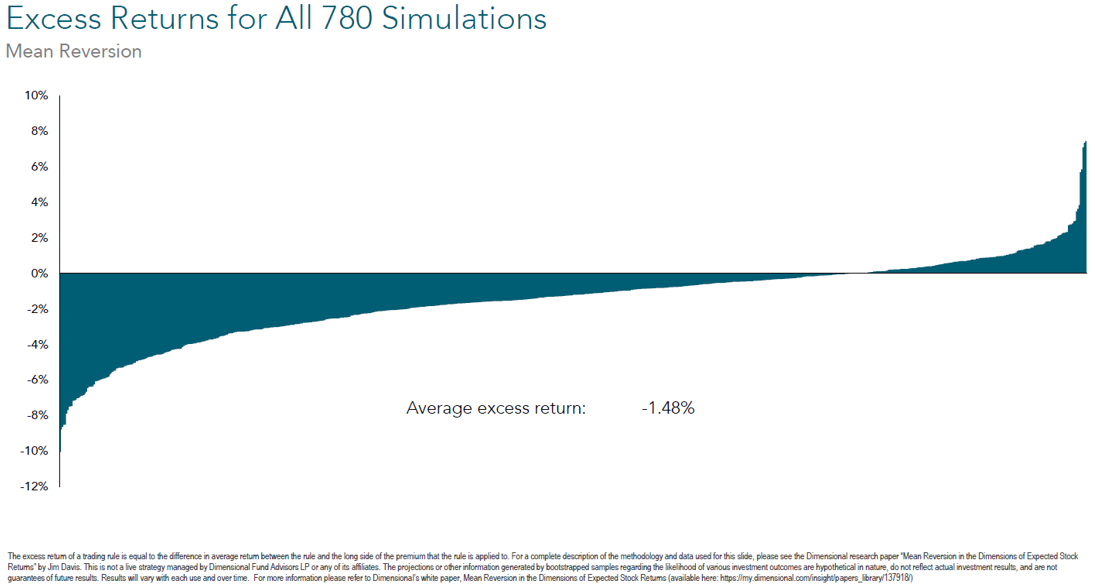

Logically, this sounds possible, and it’s certainly alluring. You could just choose a P/E ratio of, say, 18, and determine that everything above it is too expensive. You could then sell stocks when ratios are above that level and buy when they’re below. Many experiments have been conducted to try and outperform with this method.

Unfortunately, the results have not been encouraging. Only a few out of the hundreds of simulations managed to outperform a simple buy and hold approach. On average, the excess return you may receive from this ratio is negative – and that does not even take into account the possible transaction costs you will incur from trading.

3. When is Stock Market Valuation Worst?

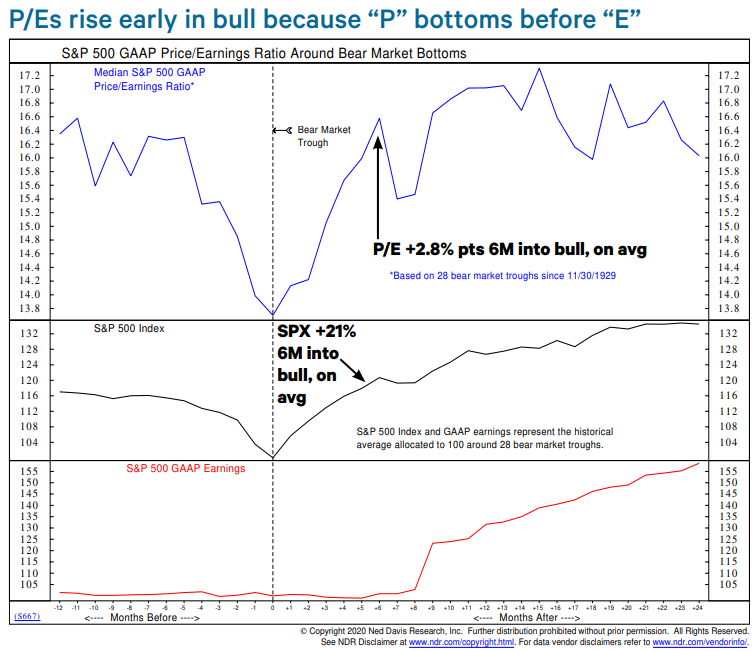

Stock market valuations are always at their worst after the stock market bottoms. In that period and during the first six months of all bull markets, regardless of recessions, the average gain is 20.7%. But as earnings continue to decline, the P/E rises 2.8% points on average, as the diagram below shows.

As such, taking action to sell when news is bad or getting worse would mean that you are transacting at the worst periods of the market, and will significantly harm your long term investments.

4. Do These Billionaires or Experts Know You?

This is, by far, the most important question. All those eminent market strategists, hedge fund managers and billionaires don’t know you. They don’t care about your risk tolerance, time horizon, financial plan or investable assets. They have billions to lose, which is most likely not the case for you. Furthermore, many of these money managers are only concerned with 1-year time horizons, as their yearly performance would make or break their careers. As such, the risk and mitigation measures they take would be vastly different from what you should do with a much longer time horizon. It would be foolish and dangerous for you to blindly mimic their moves!

This is something we have written about before. Even listening to well-meaning friends and family is not ideal, as they usually won’t have enough information or experience to make a proper assessment. Instead, stick to the investment plan that your fiduciary advisor created for you after a thorough exploration of your financial situation and goals.

Many factors contribute to how a recession could impact earnings, multiples and the market – as well as how the three tend to unfold as the economy recovers. COVID-19 has also brought a lot of uncertainty around the magnitude and timing of any recession and what its impact on the stock market would be. However, academic research and principles show that it is impossible to predict when that would happen, let alone how to time your entry and exit in the markets in order to take advantage of it.

Instead, systematic rebalancing of your portfolio in conjunction with a well-thought-out investment plan will give you the best chance for investment success in the long run.

Listening to anyone else could thus be detrimental to your financial health!

#

If you have found this article useful and would like to schedule a complimentary session with one of our advisers, you can click the button below or email us at customercare@gyc.com.sg.

Share

IMPORTANT NOTES: All rights reserved. The above article or post is strictly for information purposes and should not be construed as an offer or solicitation to deal in any product offered by GYC Financial Advisory. The above information or any portion thereof should not be reproduced, published, or used in any manner without the prior written consent of GYC. You may forward or share the link to the article or post to other persons using the share buttons above. Any projections, simulations or other forward-looking statements regarding future events or performance of the financial markets are not necessarily indicative of, and may differ from, actual events or results. Neither is past performance necessarily indicative of future performance. All forms of trading and investments carry risks, including losing your investment capital. You may wish to seek advice from a financial adviser before making a commitment to invest in any investment product. In the event you choose not to seek advice from a financial adviser, you should consider whether the investment product is suitable for you. Accordingly, neither GYC nor any of our directors, employees or Representatives can accept any liability whatsoever for any loss, whether direct or indirect, or consequential loss, that may arise from the use of information or opinions provided.