Market Sell-Off: Panic or Opportunity?

10 March 2020

“The true investor welcomes volatility. A wildly fluctuating market means that irrationally low prices will periodically be attached to solid businesses.”

— Warren Buffett

Stock markets around the world had a big sell-off on Monday, 9 March 2020. Over the last two weeks, global stocks are down over -15%. This isn’t big in the historical sense (stocks were down -50% during the dotcom bust, and -57% during the 2008 Great Financial Crisis). However, the speed at which the recent sell-off occurred was akin to a market crash. The big problem that investors always face during a crash is that it feels too late to sell, but too early to buy.

In trying to find explanations for the sell-off, the media pointed to the oil price war (between Russia and Saudi Arabia) as a cause for the rout. This may be true to some extent. A lot of financial risk models include an oil price collapse as part of a negative scenario analysis. However, the computers that do the algorithmic trading these days failed to discern that the oil price collapse wasn’t due to tanking demand, but the collapse of the oil cartel that was artificially propping up oil prices.

You could argue that demand would likely come-off, thanks to the lack of activity from the coronavirus epidemic. But what most people forget was that the global economy was actually gaining ground and on solid footing right up till Jan 2020 when the coronavirus spun out of control in China.

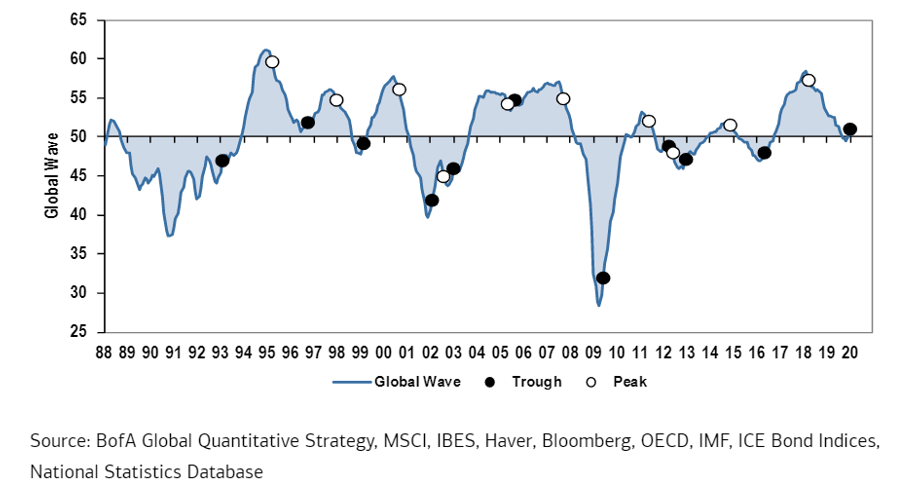

Once the fear over the virus subsides with effective treatment and containment measures, fatigue over the constant news bombardment, and a realisation that its severity is lower than past pandemics, things will be back to business as usual (take Singapore as a case in point). Multiple economic models have been confirming a rebound, and the chart below, built of various leading indicators, showed that the global economy hit a trough sometime in 3Q 2019 in the midst of the China/US trade war.

Effect on your portfolios

So, how have your portfolios been faring? First, you need to look past the scary headline numbers being bandied around in the news. The effect on your investments would be vastly different, especially if you are holding a portfolio that includes bonds, and if your funds are held in SGD.

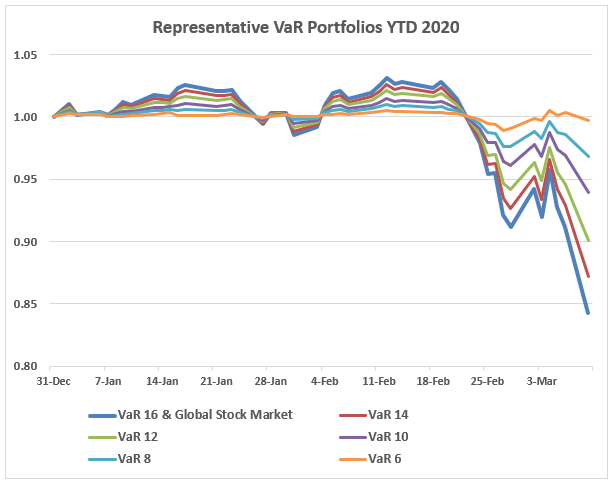

The charts below show what effect the market sell-off had on various representative portfolios, assuming all portfolios started the year with a value of 1. At the moment, all losses have been contained within their respective Value-at-Risk (VaR) metric. Global stocks and the VaR 16 portfolio (which is 100% stocks) is down approximately -16% for the year. All other portfolios are down a smaller percentage of that. For example, the VaR 10 portfolio (50% stocks and 50% bonds) is only down around -6%. (Note that the figures below are gross of any fees).

What actions have we taken?

As communicated in our email about a week ago, we undertook a rebalancing exercise after stock prices fell. Following any further sell-offs, we will initiate another rebalancing exercise to fortify your portfolio. This may include systematically selling bonds which have risen in price, or buying equities that have fallen. This ensures that your investments will be well-placed to benefit from the eventual market rebound. It will also help to reallocate risk appropriately within your portfolio and ensure that your asset allocation is not unduly skewed.

Financial stress and risk indicators – What are they telling us?

We are always concerned about whether there are underlying indicators that highlight undue market stress, as this could lead to further declines. At the moment, all the indicators that we are monitoring daily show no signals of heightened financial stress, apart from the flight of money from risky assets to perceived safe havens like bonds and cash. Central banks have been very active in ensuring that they provide liquidity in overnight lending markets to prevent any financial institution from seizing up. These are supportive and positive signals.

What is the likely outcome from this sell-off?

You only need to look back as recently as 2016 to guess the probable conclusion of this market sell-off that’s purportedly from the collapse in oil prices. In 2016, the sell-off was also mainly caused by a collapse in commodity and oil prices. Many oil companies and commodity firms operating on thin margins went bust, and investors who were overly concentrated in certain equity and high yield bond markets suffered drastic losses.

This is where the value of diversification comes in. The energy sector forms only a 4.5% allocation in a diversified global stock market portfolio. As our clients, you are not unnecessarily exposed to or concentrated in a handful of companies. In 2016, despite the negative news on the BREXIT vote and US Presidential Elections, markets ended the year on a positive note. Investors who panicked and sold early were unable to recover their losses.

What About a Recession?

If you are still worried that we might be facing a possible recession, check out our handy guide on how to prepare for a recession. It is easier than you think, and does not involve selling off all your investments.

A Great Opportunity – Don’t miss this sale!

As Warren Buffett said, a true long-term investor actually welcomes volatility, as it presents a fantastic opportunity to buy when prices are low. Any market dislocation is a tremendous wealth creation opportunity. Following the sell-off, equity prices are back to Jan 2019 and even Aug 2017 levels. Investors who missed out on the previous rally now have the chance to allocate to the market.

Essentially, Black Friday sales have come early this year!

#

If you have found this article useful and would like to schedule a complimentary session with one of our advisers, you can click the button below or email us at customercare@gyc.com.sg.

Share

IMPORTANT NOTES: All rights reserved. The above article or post is strictly for information purposes and should not be construed as an offer or solicitation to deal in any product offered by GYC Financial Advisory. The above information or any portion thereof should not be reproduced, published, or used in any manner without the prior written consent of GYC. You may forward or share the link to the article or post to other persons using the share buttons above. Any projections, simulations or other forward-looking statements regarding future events or performance of the financial markets are not necessarily indicative of, and may differ from, actual events or results. Neither is past performance necessarily indicative of future performance. All forms of trading and investments carry risks, including losing your investment capital. You may wish to seek advice from a financial adviser before making a commitment to invest in any investment product. In the event you choose not to seek advice from a financial adviser, you should consider whether the investment product is suitable for you. Accordingly, neither GYC nor any of our directors, employees or Representatives can accept any liability whatsoever for any loss, whether direct or indirect, or consequential loss, that may arise from the use of information or opinions provided.