Why investment fads can be harmful to your wealth

29 November 2019

“Insanity: Doing the same thing over and over again and expecting different results.”

—Anonymous

When was the last time someone pitched a new investment idea to you? Did you end up investing in it?

Investment fads have been around for a long time. Financial institutions know that humans are drawn to novelty. We get excited about investment ideas that resonate with the hot topics in the news.

This gives banks and fund managers the opportunity to develop and pitch investment strategies that ride on that excitement and lure us to invest. They may tempt investors with the perceived opportunities in certain countries, regions, technological changes, or the scarcity of natural resources. Perhaps they might toss in a free gift or bonus units to sweeten the deal. After all, enticing you to invest is how they earn their commissions.

There is nothing wrong with all this… provided you have the money to gamble with.

Nobel laureate Eugene Fama once said, “There’s one robust new idea in finance that has investment implications maybe every 10 or 15 years, but there’s a marketing idea every week.”

In the early 90’s, a lot of attention turned to the “Asian Tigers” of Hong Kong, Singapore, South Korea and Taiwan. But the 1997 Asian financial crisis put a dampener on many investments in these countries, and then took a long time to recover.

A few years later, much was written about the emergence of the “BRIC” countries of Brazil, Russia, India and China and their growing influence in global markets. Whilst China (and to a smaller extent, India) are still doing relatively well, the other countries have fallen by the wayside. Goldman Sachs, whose former famous economist Jim O’Neill coined the popular BRIC phrase, has quietly closed its BRIC fund after losing more than 88% of the assets.

Goldman Sachs then came up with the trendy term, the “Next Eleven”, which they identified as the next 11 countries that would follow the BRIC economies onto the world stage. The fund, which was wildly popular in 2013 and 2014, has since sputtered out. It could only be a matter of time before the strategy is shelved or merged with something else.

Funds targeting hot industries or trends have come into and fallen out of vogue time and time again. In the 1950s, the “Nifty Fifty” were all the rage. In the 60’s, go-go stocks and funds piqued investor interest. In the 20th century, money poured into funds poised to “make the most” out of the IT and telecommunication services – resulting in the dotcom boom. Following the stock market collapse of 2008, “Black Swan” funds, “tail-risk hedging” strategies and “liquid alternatives” abounded. In recent times, investments focusing on micro-lending, peer-to-peer lending, cryptocurrencies and cannabis cultivation have come to the fore. You may have also been caught up in the whole FAANG (Facebook, Apple, Amazon, Netflix & Google) stock frenzy a short time back.

In this low interest rate environment, investors hungry for yield have also piled into income-focused funds, such that multi-asset, unconstrained bond funds, and asset-backed funds have proliferated to meet this huge demand. More recently, an article by The Business Times shone the spotlight on thematic funds – a new breed of strategies dreamt up by fund managers which invests into very concentrated and narrow themes like water, robotics or cyber-security. Due to its narrow focus and the sheer unpredictability of world and market trends, the probability of any of these funds succeeding cannot be very high.

Whilst it is always easy on hindsight to point out the obvious fortune one could have made by making a specific market call, trying your luck based on that is like trying to drive forward by looking at the rear view mirror. It is more than likely you would meet with an accident!

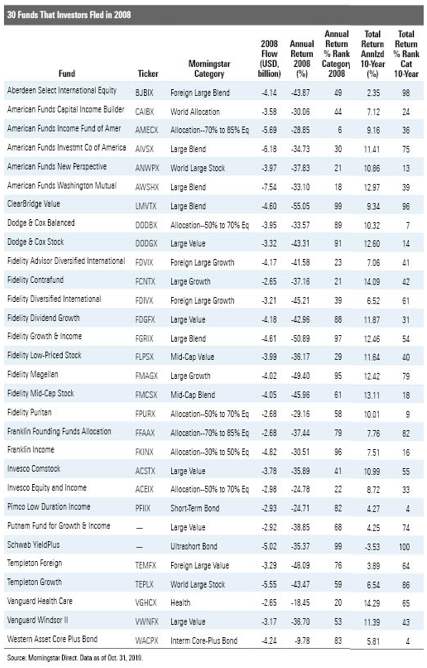

The overwhelming evidence actually shows the futility in trying to identify such mispricing in advance and reliably profit from it. For example, a large proportion of investment strategies fail to survive over the long term. Out of 1,622 bond funds in existence in 2004, only 55% remain. Similarly, amongst equity funds, only 51% of the 2,786 funds survived. Those are terrible odds for monies you cannot afford to lose! It’s like tossing a coin to see whether all your monies will evaporate or not. A Morningstar report (see diagram below) shows some popular funds in 2007 and its subsequent 2008 performance and how investors fled from them. Although some have come back over the ten-year period since the 2008 financial crisis, many are still languishing far behind.

When you are faced with the choice as to whether to add new types of assets or strategies into your existing investments, it is helpful to ask the following questions:

- What is this strategy claiming to provide that is not already in my portfolio?

- If it is not in my portfolio, can I expect it to increase my returns, or reduce my risk or volatility?

- If it is not in my investments, can including it help me to achieve my goals more quickly?

- Am I comfortable with the possibility of it performing poorly and losing all my money?

If you have any doubts about the answers to these questions, it would be wise to exercise caution before buying. The time-tested and evidence-based strategy for investing in stocks is using a market or asset class fund that will expose you to thousands of companies doing business around the world, and which is broadly diversified across industries, sectors and countries. Working with a fiduciary advisor will help individuals and even families to create a customised investment plan that fits their needs and risk appetites.

There will always be exciting new investment ideas that will entice investors to part with their monies. Take the gamble if you like with money that you can afford to lose. But for the more critical financial objectives like ensuring sufficient funds to last your retirement years, you will want an outcome that has the highest probability of success; and that is an evidence-based one.

#

If you have found this article useful and would like to schedule a complimentary session with one of our advisers, you can click the button below or email us at customercare@gyc.com.sg.

Share

IMPORTANT NOTES: All rights reserved. The above article or post is strictly for information purposes and should not be construed as an offer or solicitation to deal in any product offered by GYC Financial Advisory. The above information or any portion thereof should not be reproduced, published, or used in any manner without the prior written consent of GYC. You may forward or share the link to the article or post to other persons using the share buttons above. Any projections, simulations or other forward-looking statements regarding future events or performance of the financial markets are not necessarily indicative of, and may differ from, actual events or results. Neither is past performance necessarily indicative of future performance. All forms of trading and investments carry risks, including losing your investment capital. You may wish to seek advice from a financial adviser before making a commitment to invest in any investment product. In the event you choose not to seek advice from a financial adviser, you should consider whether the investment product is suitable for you. Accordingly, neither GYC nor any of our directors, employees or Representatives can accept any liability whatsoever for any loss, whether direct or indirect, or consequential loss, that may arise from the use of information or opinions provided.