Investing, Like Life, Is Always Uncertain

09 November 2018

If you have been investing for some time, this saying may be familiar to you: “I’m not sure where the market is going, so I’ll stay out until it becomes clearer”. Or how about: “I’ve made some money in the market and now things seem uncertain, so maybe it’s a good time to sell and wait on the sidelines.” But when has investing – or life for that matter – ever been so clear?

Imagine that you knew exactly what would happen to you from the day you were born. You knew exactly what exam scores you would achieve, knew exactly which company and job you would work at, who you would marry, how many children you would have, where they would go and study, what house you would live in, what vacations you would take, and when you would die. Wouldn’t life be dreary and mind-numbing if you knew exactly what was going to happen next? Is that how you would want to live your life?

Investing is the same. The reason you are paid a return is that it is compensation for the risk you take for the uncertainties in participating in capital markets. So, why then do so many people demand certainty when they invest? If there were absolute certainty – that is, no risk whatsoever – there would be no returns. Because who would give you something for taking no risk?

Knee-jerk, emotion-driven swings often happen because of the scary things investors see happening in the markets, but there is no need to panic. The world has gone through decades of major and minor events. While investors may have suffered short-term losses through some of these events, everything still worked out well in the long term.

Take for example, the deep uncertainty which clouded the investing universe in March 2009, some 9 years ago. There were those who were convinced that the stock market had bottomed, and the case for an upturn was convincing. Stock trading volumes were up, economic recession indicators were easing, banks were slowly turning a profit, and commodity prices (often a sign of demand) had bounced.

But there were also those who had convincing arguments that the pain would continue. Banks still had a huge bulk of toxic mortgage assets on their balance sheets, economic signs were still not strong enough, short-covering was presumably driving the rallies, ponzi schemes like the Bernie Madoff scandal affected confidence, and fear was very much widespread. At that time, many retail investors had also sold out of the market (at the worst possible time), fearing the collapse of the global financial system.

In actual fact, March 2009 marked the end of the great financial crisis, and in that year alone, stocks staged a spectacular recovery. Over the following years, stocks eventually clawed their way back. But investors who had gotten out, or never stepped in, either realised substantial losses or missed out on making their money work harder.

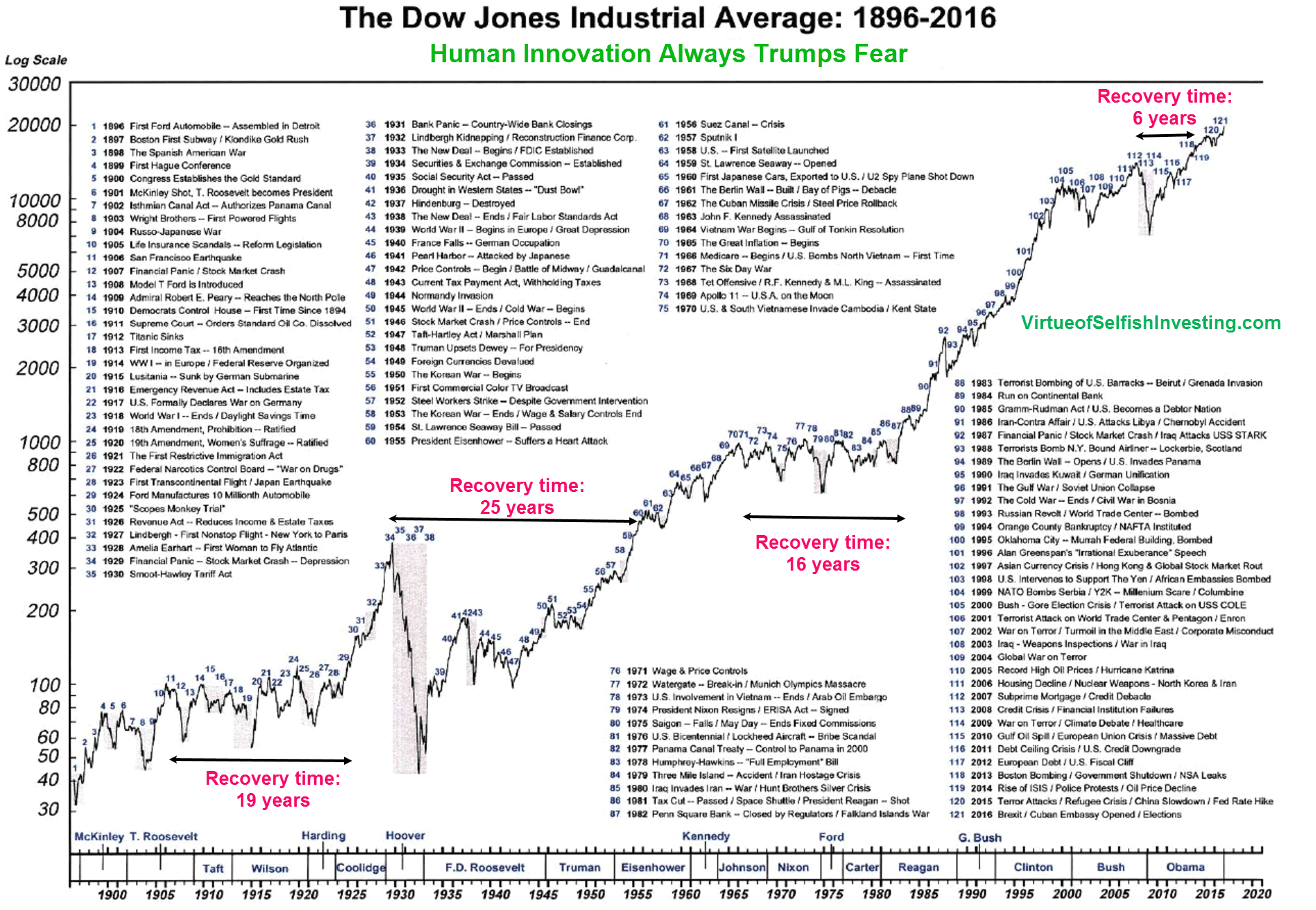

However, the post-2009 market recovery years were also marked by periods of major uncertainty. The US was downgraded from being a AAA-rated economy, and racked with frequent brinkmanship over the debt ceiling and rancorous politics. Europe and “PIGS” (Portugal, Ireland, Greece and Spain) were entwined in a sovereign debt crisis. China grappled with an economic slowdown as it transitioned from an export-led to a domestic-driven services economy. Commodities went through a bear market with many oil and gas companies going bust. The extremely old Dow Jones Index, one of the oldest stock market indices in the world (large version here), shows the many financial crisis, wars, legislations, terrorist activities, significant economic events and political events that hit the markets over the last century. It is important to note that throughout all the major and cyclical bear cycles, in the end, the stock market always ended up.

In the midst of all these events, market strategists, economists and financial experts will always provide us with a diverse range of reasons as to what happened and an equally diverse breadth of solutions for investors to take action on.

The pertinent question for us is: what should we do with all this information? The fact that professionals “agree to disagree” and struggle to accurately forecast the future shows that nobody, even super-qualified experts, are able to predict the outcome of markets. History suggests that investors who are looking for “certainty” before investing are likely to set themselves up for a long wait. There is no shortage of events that affect the world every day. Will things ever calm down and become certain? The obvious short answer is, ‘No’.

So, what should investors do?

1. Invest for Goals

Rather than invest with the objective of trying to beat the market, and to time the best opportunity to buy and sell, a better and more stress-free way would be to invest according to the goals you need to meet. Whether your goal is to achieve $1M or $4M at retirement, proper planning and matching of a suitable risk/return portfolio will help you focus on the long term target. Whether or not the market moves up or down in the next 6 months is then moot in the context of your final objective.

2. Systematic Market Timing

Whilst we regularly say that no one can time the market and predict what is happening, there is still a systematic way to sell high and buy low. This would be through a concept called rebalancing.

If you had a properly constructed portfolio with a percentage in stocks and bonds, and stocks had risen a considerable amount after a rally, it means that your original allocation is out of sync. Rebalancing ensures that you sell a portion of your stocks (which have risen in price) to buy into bonds (whose prices are relatively lower). This automatically locks in profits from your stocks.

It is the same when you suffer a market collapse and stock prices go down a considerable amount. Since the allocation is out of sync, you sell your bonds to buy into stocks (which are low in price) to bring your portfolio back to its original allocation. Viola! A systematic way to sell high and buy low, repeated ad infinitum.

3. Proper Diversification

If you saw the long-term Dow Jones chart above, you would have noticed that some events affected the US, some affected Europe or Middle-East, and some Asia. Is it possible to pre-empt these events by moving your investments around the different regions of the world? The truth is that it is near impossible to do so, regardless of what fund managers may say. Plus, you would end up saddled with high transaction costs from frequent buying and selling with dubious benefits.

So, how do investors prevent their portfolio from being affected by a large event that occurs in one or a few countries? By simply diversifying their investments throughout the world. In doing so, you automatically ensure that you are not affected by a single event that could wipe out your investments, and you are not affected by the opinions of media and market pundits about what is happening in the short term.

To conclude, investors should remember that you read or watch the news for what it is: information. It is also good to be aware of what is happening around the world. But, more importantly, just as there are opinion pieces about politics, the weather and everything else under the sun, you should likewise treat opinions about where to invest with a pinch of salt and for entertainment purposes. This prevents you from meddling with your long-term investment strategy and thus helps you avoid the illusion that somewhere, somehow, certainty will return.

#

If you have found this article useful and would like to schedule a complimentary session with one of our advisers, you can click the button below or email us at customercare@gyc.com.sg.

Share

IMPORTANT NOTES: All rights reserved. The above article or post is strictly for information purposes and should not be construed as an offer or solicitation to deal in any product offered by GYC Financial Advisory. The above information or any portion thereof should not be reproduced, published, or used in any manner without the prior written consent of GYC. You may forward or share the link to the article or post to other persons using the share buttons above. Any projections, simulations or other forward-looking statements regarding future events or performance of the financial markets are not necessarily indicative of, and may differ from, actual events or results. Neither is past performance necessarily indicative of future performance. All forms of trading and investments carry risks, including losing your investment capital. You may wish to seek advice from a financial adviser before making a commitment to invest in any investment product. In the event you choose not to seek advice from a financial adviser, you should consider whether the investment product is suitable for you. Accordingly, neither GYC nor any of our directors, employees or Representatives can accept any liability whatsoever for any loss, whether direct or indirect, or consequential loss, that may arise from the use of information or opinions provided.

{kind=link}