Should Investors Sell After a “Correction”?

26 September 2015

By Weston Wellington, Vice President, Dimensional Fund Advisors

Stock prices in markets around the world fluctuated dramatically for the week ended August 27. On Monday, August 24, the Dow Jones Industrial Average fell 1,089 points—a larger loss than the “Flash Crash” in May 2010—before rallying to close down 588. Prices fell further on Tuesday before recovering sharply on Wednesday, Thursday, and Friday. Although the S&P 500 and Dow Jones Industrial Average rose 0.9% and 1.1%, respectively, for the week, many investors found the dramatic day-to-day fluctuations unsettling.

Based on closing prices, the S&P 500 Index declined 12.35% from its record high of 2130.82 on May 21 through August 24. Financial professionals generally describe any decline of 10% or more from a previous peak as a “correction,” although it is unclear what investors should do with this information. Should they seek to protect themselves for further declines by selling, or should they consider it an opportunity to purchase stocks at more favourable prices?

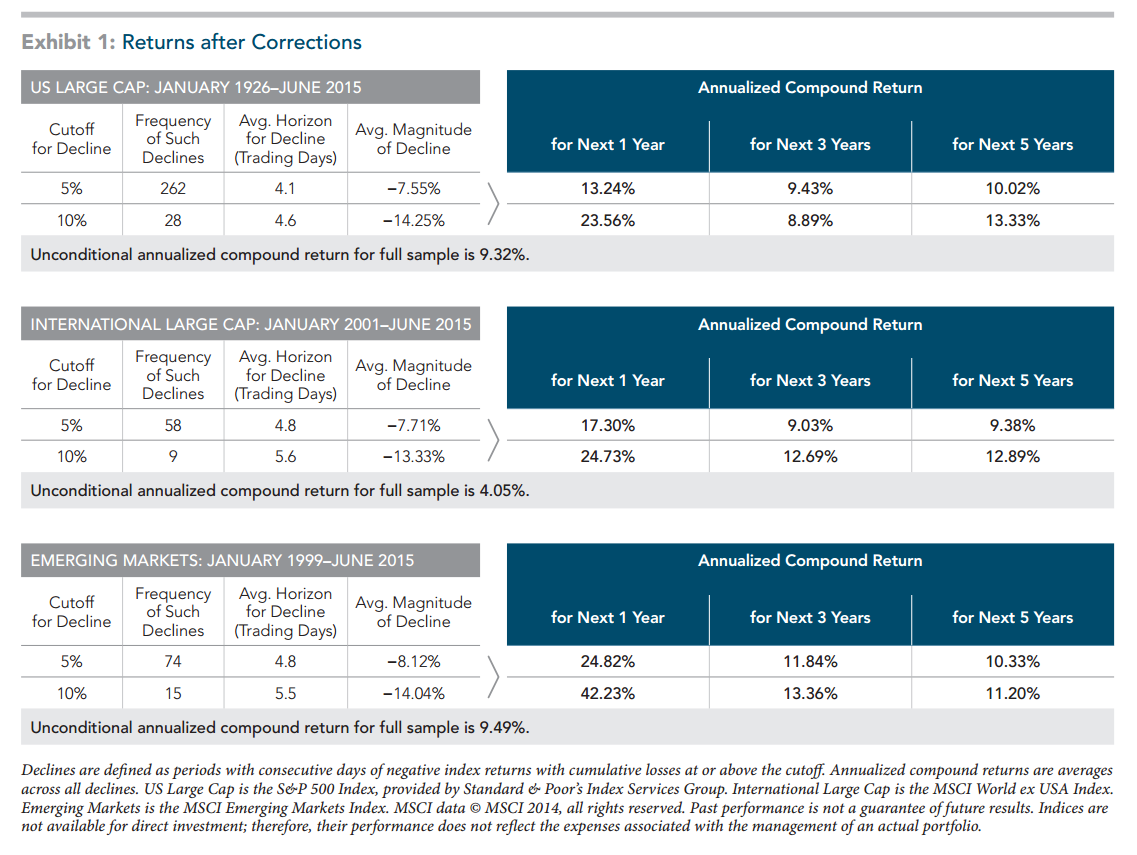

Based on S&P 500 data, stock prices have declined 10% or more on 28 occasions between January 1926 and June 2015. Obviously, every decline of 20% or 30% or 40% began with a decline of 10%. As a result, some investors believe that avoiding large losses can be accomplished easily by eliminating equity exposure entirely once the 10% threshold has been breached.

Market timing is a seductive strategy. If we could sell stocks prior to a substantial decline and hold cash instead, our long-run returns could be exponentially higher. But successful market timing is a two-step process: determining when to sell stocks and when to buy them back. Avoiding short-term losses runs the risk of avoiding even larger long-term gains. Regardless of whether stock prices have advanced 10% or declined 10% from a previous level, they always reflect (1) the collective assessment of the future by millions of market participants and (2) the expectation that equities in both the US and markets around the world have positive expected returns.

Exhibit 1 below shows that US stocks have typically delivered above-average returns over one, three, and five years following consecutive negative return days resulting in a 10% or more decline. Results from non-US markets are similar.

Source: Dimensional Fund Advisors

Contrary to the beliefs of some investors, dramatic changes in security prices are not a sign that the financial system is broken but rather what we would expect to see if markets are working properly. The world is an uncertain place. The role of securities markets is to reflect new developments— both positive and negative—in security prices as quickly as possible. Investors who accept dramatic price fluctuations as a characteristic of liquid markets may have a distinct advantage over those who are easily frightened or confused by day-to-day events, and are more likely to achieve long-run investing success.

REFERENCES

- “Wild Ride Leaves Investors Grasping,” Wall Street Journal, August 25, 2015.

- “Investors Scramble as Stocks Swing,” Wall Street Journal, August 25, 2015.

#

If you have found this article useful and would like to schedule a complimentary session with one of our advisers, you can click the button below or email us at customercare@gyc.com.sg.

Share

IMPORTANT NOTES: All rights reserved. The above article or post is strictly for information purposes and should not be construed as an offer or solicitation to deal in any product offered by GYC Financial Advisory. The above information or any portion thereof should not be reproduced, published, or used in any manner without the prior written consent of GYC. You may forward or share the link to the article or post to other persons using the share buttons above. Any projections, simulations or other forward-looking statements regarding future events or performance of the financial markets are not necessarily indicative of, and may differ from, actual events or results. Neither is past performance necessarily indicative of future performance. All forms of trading and investments carry risks, including losing your investment capital. You may wish to seek advice from a financial adviser before making a commitment to invest in any investment product. In the event you choose not to seek advice from a financial adviser, you should consider whether the investment product is suitable for you. Accordingly, neither GYC nor any of our directors, employees or Representatives can accept any liability whatsoever for any loss, whether direct or indirect, or consequential loss, that may arise from the use of information or opinions provided.